Introduction

Possession is often described as nine-tenths of the law, but in the complex intersection of insolvency and debt recovery, the remaining one-tenth of ownership is where the fiercest battles are fought. This article delves into the critical timing of legal protections, specifically whether a personal insolvency moratorium can halt the final handover of property after a successful bank auction. The core issue of discussion in the article is whether the amendment to Section 13(8) of the SARFAESI Act1, which limits the right of redemption to the date of auction notice, also results in the immediate extinguishment of the borrower’s ownership rights.

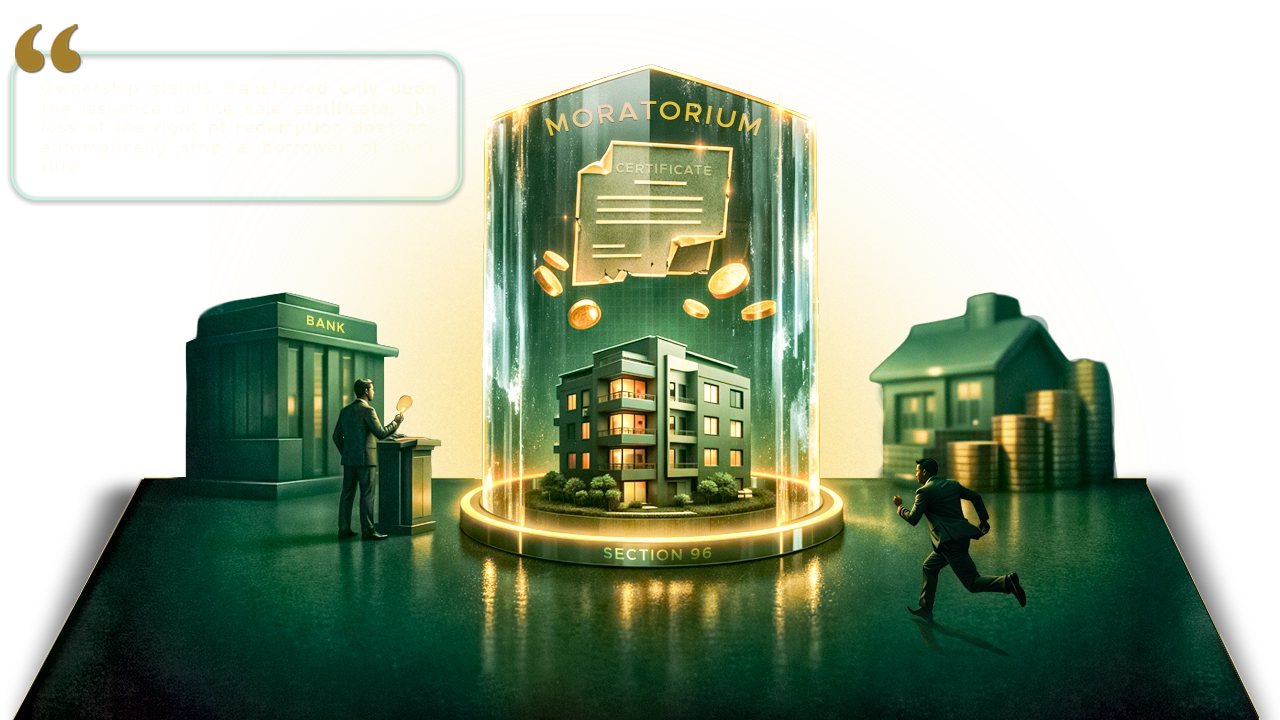

The focus of new age jurisprudence lies in the statutory supremacy of the IBC2 versus the streamlined recovery mechanisms of the SARFAESI Act. Primarily, the High Court of Judicature at Bombay, coram R.I. Chagla and Farhan P. Dubash, JJ., in the matter of Arrow Business Development Consultants Pvt. Ltd. Vs. Union Bank of India & Ors3., held that if a sale certificate is not issued and the full price not paid before an interim-moratorium under Section 96 of the IBC kicks in, the ownership remains with the borrower, thus staying further proceedings.

The Respondent Bank classified the Borrowers’ account as an NPA4 and subsequently took symbolic possession of their residential flat. An auction was conducted, where the Petitioner was declared the successful bidder; however, before the full sale consideration was paid and the sale certificate issued, one of the co-borrowers filed for personal insolvency under Section 94 of the IBC. This filing triggered an interim-moratorium, yet the Bank proceeded to accept the balance payments and issued a sale certificate.

Redemption vs. Ownership: Decoding the Scope of Interim-Moratorium

The Petitioner, as the auction purchaser, argued that the Borrowers’ right, title, and interest were extinguished the moment the auction notice was issued or, at the latest, when the auction was confirmed. Relying on the amended Section 13(8) of the SARFAESI Act, they claimed that since the right to redeem the mortgage was lost before the IBC application was filed, the interim-moratorium could not apply to a property that effectively no longer belonged to the Borrowers.

On the other hand, the RP5 and the Borrowers contended that the interim-moratorium under Section 96 is expansive and “stays” all legal actions regarding the debt. They argued that ownership of immovable property only transfers upon the issuance of a sale certificate and registration. Since the moratorium began before the sale certificate was only issued on June 20, the Bank’s actions in accepting further money and finalizing the sale were illegal and void.

The Court analyzed the shift in the law following the 2016 Amendment to Section 13(8) of the SARFAESI Act, comparing it with established precedents.

“Ownership of immovable property stands transferred only upon the issuance of the sale certificate and the 2016 Amendment… does not alter this position since the equity of redemption is only a facet of rights that constitutes ownership.”

The Court examined the Supreme Court’s decision in Celir LLP v. Bafna Motors (Mumbai) (P) Ltd6., which clarified that the right of redemption is lost once the sale notice is published. However, the Court distinguished this from the transfer of title. It placed heavy reliance on Indian Overseas Bank v. RCM Infrastructure Ltd7., where the Apex Court held that if the sale process (specifically the full payment and certificate issuance) is incomplete when a moratorium begins, the property remains part of the debtor’s estate. The Court noted that under the IBC, the interim-moratorium under Section 96 is wider than Section 14, as it attaches to the “debt” itself, preventing any further steps by creditors.

The Court removed the dichotomy by ruling that “right of redemption” and “ownership” are distinct legal concepts. While the 2016 Amendment prevented the Borrowers from stopping the sale by tendering dues late, it did not automatically strip them of their ownership until the sale was perfected. The interim-moratorium under Section 96 of the IBC was triggered, at a time when the Petitioner had only paid a fraction of the bid and no sale certificate existed by which a legal “freeze” was enacted. Consequently, the Bank was prohibited from accepting the remaining six tranches of payment or issuing the sale certificate. Ownership stands transferred only upon the issuance of the sale certificate; the loss of the right of redemption does not automatically strip a borrower of their title. The Court held the sale certificate issued to be non-est in the eyes of the law.

Conclusion

This case reinforces the principle that the IBC holds a prevailing position over the SARFAESI Act once insolvency proceedings are initiated. The Bombay High Court has clarified that the “race to the finish line” between an auction purchaser and a debtor filing for insolvency is won by the party who secures their legal status (either a sale certificate or a moratorium) first.

This judgment will likely lead to greater caution among secured creditors and auction purchasers. Banks will now feel immense pressure to conclude sale formalities with extreme speed to avoid the “intervening” effect of a Section 94 or 95 filing. Conversely, it provides a powerful, albeit time-sensitive, shield for individual borrowers and guarantors to protect their assets from being finalized in an auction sale if they are willing to enter the insolvency resolution process.

Can a co-owner who has not filed for insolvency still lose their 50% share of the property to a SARFAESI sale while their spouse’s share is protected by a moratorium? Does the “good faith” of an auction purchaser who pays the full amount unaware of a hidden IBC filing entitled them to a priority lien over the property? Legislative clarity is needed to define the status of “earnest money” in these scenarios; perhaps a statutory provision should allow for the immediate refund of bid amounts with market-rate interest if a sale is frustrated by a moratorium, to protect innocent third-party investors.

Citations

- Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002

- Insolvency and Bankruptcy Code, 2016

- Arrow Business Development Consultants Pvt. Ltd. Vs. Union Bank of India & Ors. (WP/11132/2025)

- Non- Performing Asset

- Resolution Professional

- Celir LLP v. Bafna Motors (Mumbai) (P) Ltd. (2024) 2 SCC 1

- Indian Overseas Bank v. RCM Infrastructure Ltd. (2022) 8 SCC 516

Expositor(s): Adv. Shreya Mishra