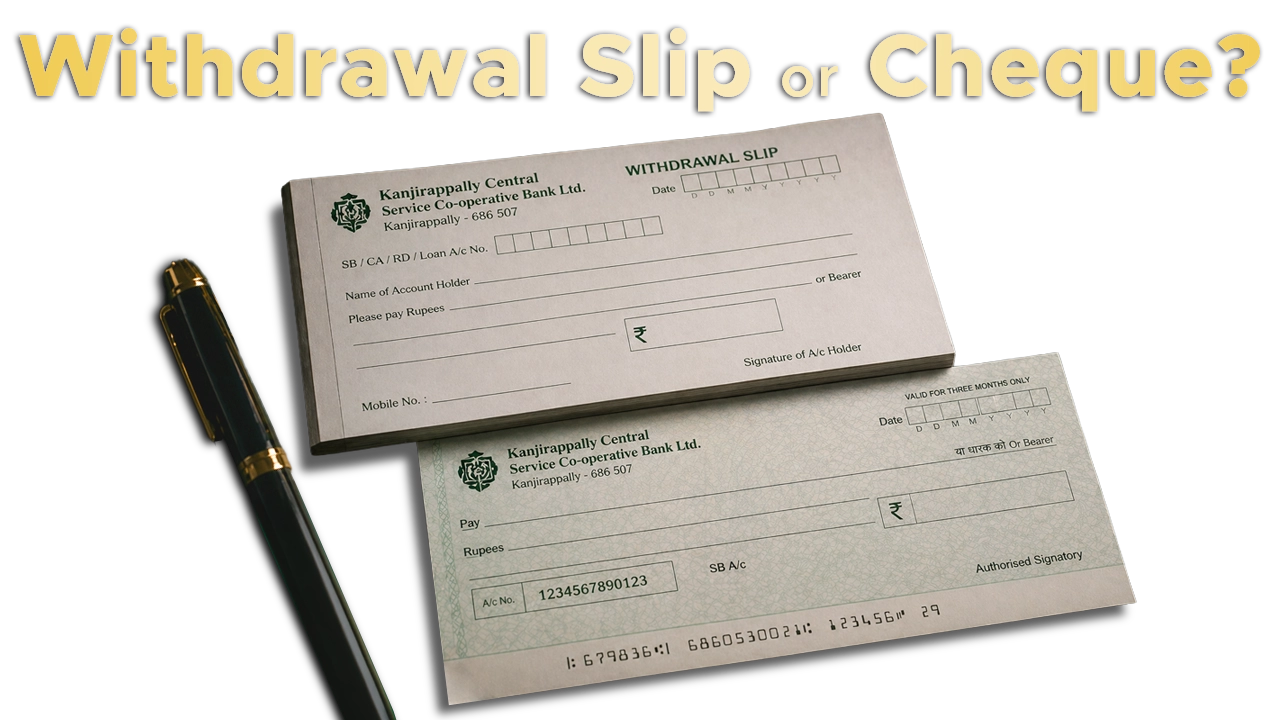

Can a mere withdrawal slip, typically an internal banking tool, trigger the criminal rigors of Section 138 of the Negotiable Instruments Act1? This pivotal question was at the heart of the Kerala High Court’s decision in Clara Dominic v. Tomy Eapen2, where the petitioner sought to quash a criminal complaint by arguing that a withdrawal slip from a co-operative society lacked the statutory character of a “cheque” and that the society itself was not a licensed banking institution. The Court answered in the affirmative, reinforcing a significant legal precedent: the definition of a “banker” is of wide amplitude, and the substance of a transaction, rather than its technical nomenclature, determines legal liability.

The factual matrix of the case centers on a dispute involving a document dated July 1, 2025, issued by the Kanjirappally Central Service Co-operative Bank Ltd. The petitioner, a 65-year-old woman, was accused in S.T. No. 5023 of 2025 after the instrument was dishonored upon presentation. She contended that the 1st respondent had surreptitiously obtained the withdrawal slip and manipulated it into a cheque, further asserting that the society was not a “banker” under Section 3 of the N.I.3 Act because it was not licensed by the Reserve Bank of India. On March 26, 2026, the High Court scrutinized these claims to determine if the foundation of the prosecution was legally untenable.

In dismissing the petitioner’s challenge, Justice C.S. Dias articulated a rationale rooted in the Doctrine of Substance over Form. This doctrine dictates that the true nature of a document is determined by its intended effect and the underlying rights it creates, rather than the label attached to it. The Court emphasized that for the purposes of the N.I. Act, the term “banker” is inclusive and extends to any institution performing banking functions, such as accepting deposits repayable on demand and providing withdrawal facilities. The judgment drew heavily from the Karnataka High Court’s ruling in Upendra Kumar v. Don Finance Corporation4, which held that instruments drawn on such institutions including withdrawal slips operating as payment mandates cannot be excluded from the sweep of the Act merely due to their name.

The Court further cited Gandhigram Agro Based Industrial Co-operative Society Ltd. v. Marangattupilly Service Co-operative Bank Ltd.5, which clarified that the essence of “banking” lies in the nature of the activity rather than the regulatory status of the institution. The mere absence of a license under Section 22 of the Banking Regulation Act6 does not strip an entity of its banking character or allow it to be used as a shield to evade legal obligations. This aligns with a broader judicial shift toward protecting the efficacy of banking operations and the acceptability of payment orders.

Ultimately, the Court mentioned that if an instrument operates as a mandate for payment drawn on an account maintained with an institution carrying on banking functions, it falls squarely within the ambit of the N.I. Act. By refusing to exercise its inherent jurisdiction to quash the proceedings under Section 528 of the Bharatiya Nagarik Suraksha Sanhita (BNSS)7, the Court signaled that the integrity of the financial system depends on holding parties accountable for the mandates they issue. While the petitioner retains the liberty to raise other defenses at trial regarding the alleged manipulation of the document, this ruling stands as a stern reminder that the law looks past the veil of nomenclature to find the heart of the obligation.

Conclusion

The Kerala High Court’s present ruling represents a pragmatic evolution in the interpretation of the Negotiable Instruments Act. By prioritizing the substance of the transaction over the technical label of the document, the Court has effectively closed a potential loophole that might have allowed individuals to evade liability simply by using non-traditional banking instruments. This decision reinforces the idea that any mandate for payment issued to a functional banking entity carries the weight of a legal promise, ensuring that the spirit of Section 138 to maintain the credibility of financial transactions remains intact.

The ruling underscores a critical judicial philosophy: the law will not permit technicalities to undermine financial accountability. Whether an instrument is titled a “cheque” or a “withdrawal slip,” its function as a vehicle for debt discharge is what triggers statutory consequences. Consequently, the High Court determined that the integrity of the credit system relies on the enforceability of payment mandates, reminding litigants that the essence of a legal obligation far outweighs the nomenclature used to describe it.

Citations

Expositor(s): Adv. Archana Shukla