The rules of the Bar Council of India prohibit law firms from advertising and soliciting work through communication in the public domain. This website is meant solely for the purpose of information and not for the purpose of advertising. Kings & Alliance LLP does not intend to solicit clients through this website. We do not take responsibility for decisions taken by the reader based solely on the information provided in the website. By clicking on ‘ENTER’, the visitor acknowledges that the information provided in the website (a) does not amount to advertising or solicitation and (b) is meant only for his/her understanding about our activities and who we are.

By continuing to use this site you consent to the use of cookies on your device as described in our Cookie Policy

Latest CIRP Filing Data Reveals How Financial and Operational Creditors Use the IBC

Subscribe

Share

5 min well spent

Introduction

What separates a bankruptcy framework from a routine payment-recovery lever is who uses it and for what purpose. In the early years of the Insolvency and Bankruptcy Code, 2016 (IBC), the Corporate Insolvency Resolution Process (CIRP) was often invoked in disputes that were, in substance, trade-credit payment conflicts. In many such matters, the filing served as a pressure point for settlement rather than as the opening step in a genuine insolvency-resolution process. That created a structural tension: a statute designed for collective resolution of financial distress was frequently being used in situations that resembled bilateral recovery contests.

The latest data published by the Insolvency and Bankruptcy Board of India (IBBI), however, suggests that this usage pattern is changing. The numbers now indicate a visible shift in the profile of CIRP initiators, with the filing landscape appearing increasingly financial-creditor-led.

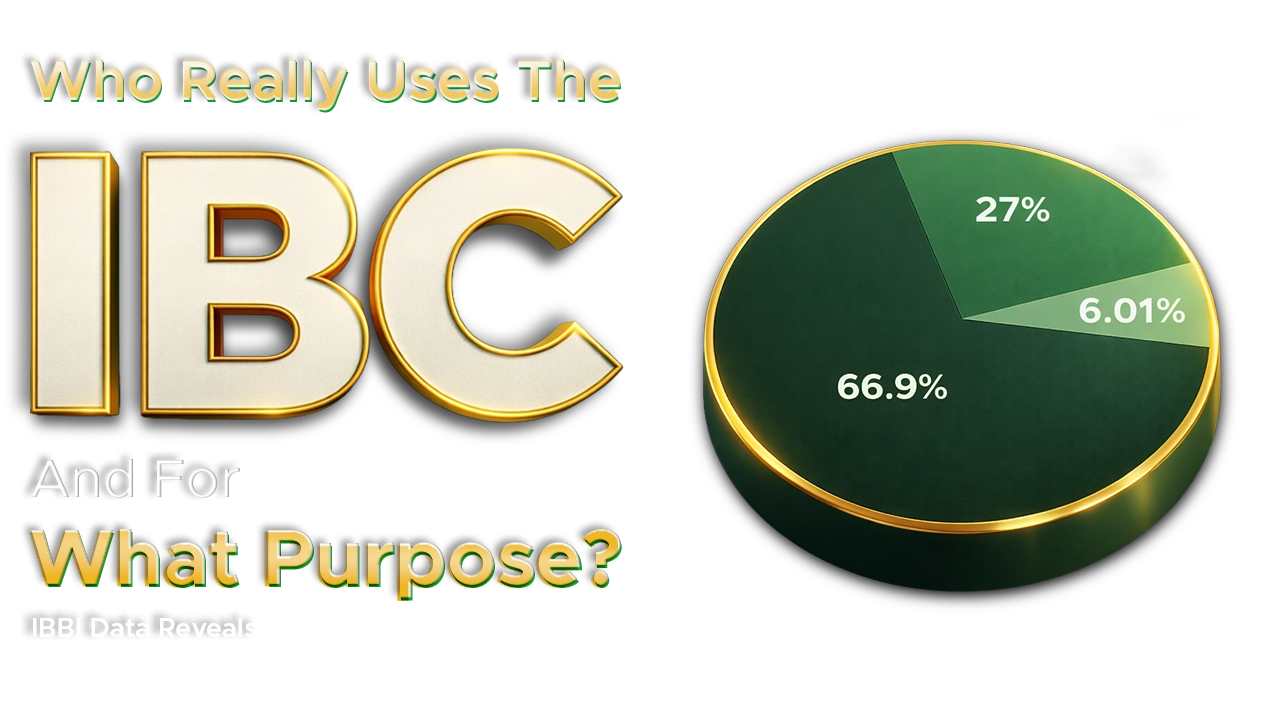

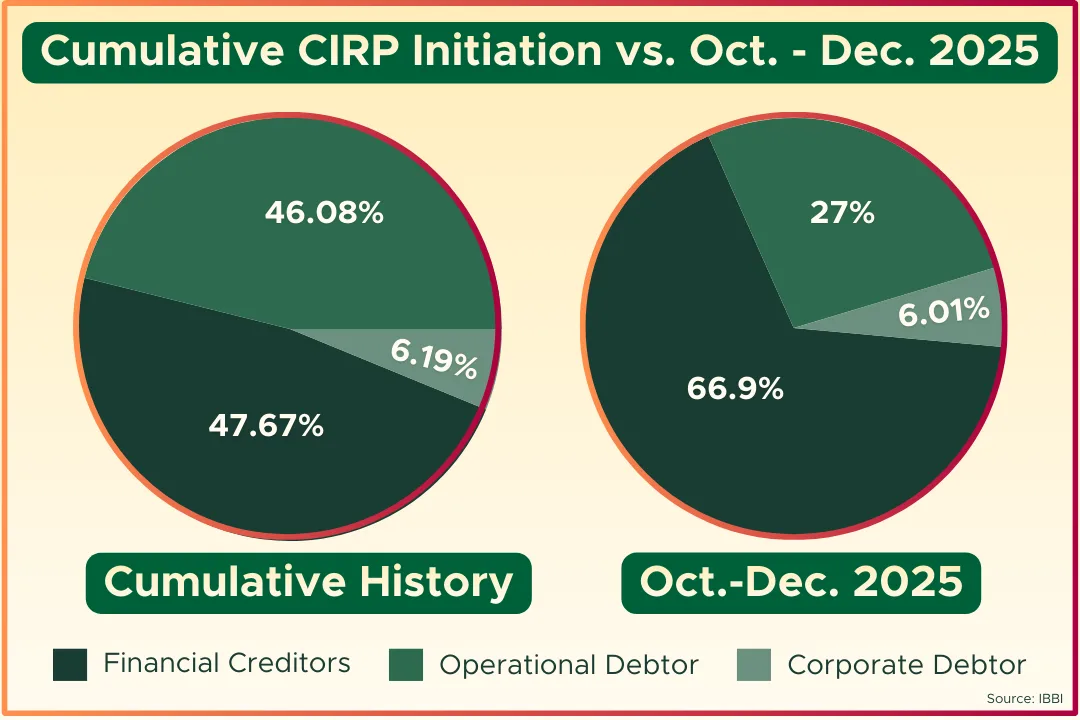

Financial Creditors Are Becoming the Dominant CIRP Users

Across the Code’s cumulative history, financial creditors (FCs) triggered 47.67% of CIRPs, operational creditors (OCs) triggered about 46.08%, and the balance came from corporate debtors (CDs).

But the position looks markedly different when one isolates the Oct–Dec 2025 quarter. During that quarter, CIRP initiations stood at 109(66.9%) by financial creditors, 44(27%) by operational creditorsand 10(6.1%) by corporate debtors. The contrast is significant. A better way to describe this development is a user-base inversion: the IBC appears to be moving from a filing landscape where FCs and OCs were nearly neck-and-neck toward one where financial creditors are becoming the dominant institutional users of the process.

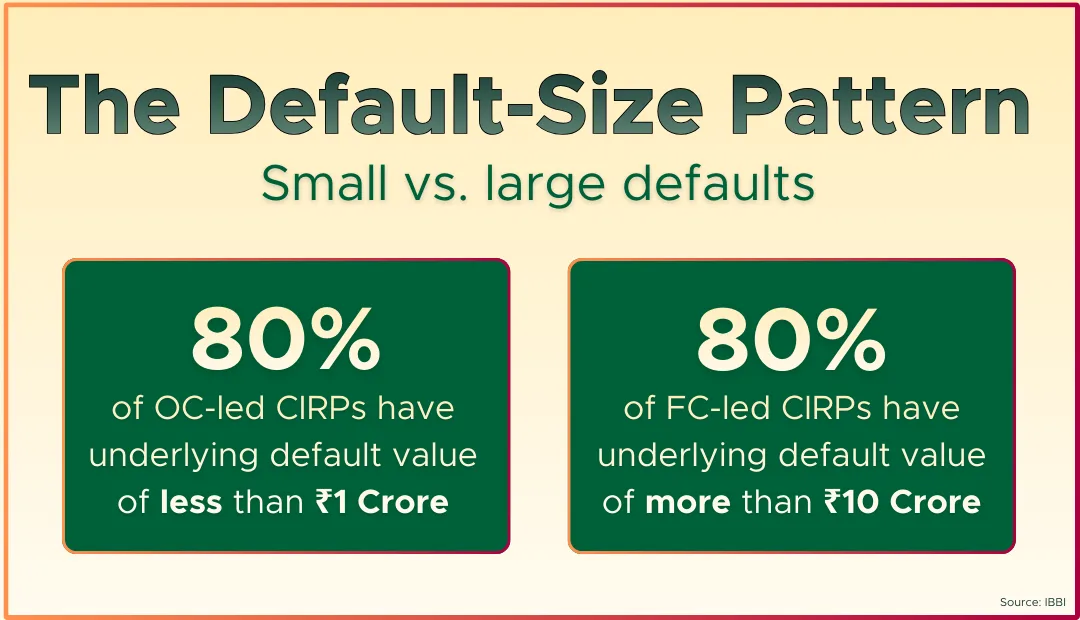

The Default-Size Pattern Behind the Shift

The IBBI newsletter does more than give quarterly totals. It also identifies a default-size pattern in stakeholder-wise initiation. About 80% of CIRPs involving an underlying default of less than ₹1 crore were initiated by operational creditors, while about 80% of CIRPs involving an underlying default of more than ₹10 crore were initiated by financial creditors. It indicates that the recent inversion in filing share is about which kinds of defaults are entering CIRP, and which creditor class is structurally more likely to initiate proceedings at each end of the default spectrum.

Initiation, however, is only one side of the story. The more revealing question is what happens to these cases once they enter the system.

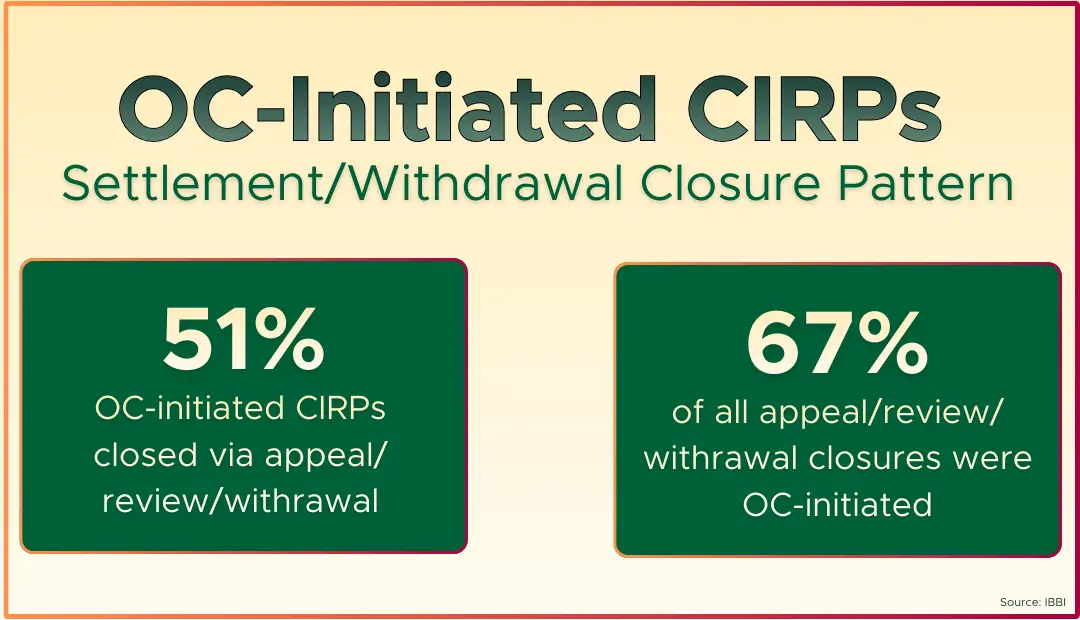

What the Closure Data Reveals About Creditor Behaviour

As of 31 December 2025, the outcome of CIRPs initiated by different stakeholders shows that OC-led matters continue to have a strong presence in closures through appeal, review, settlement, or withdrawal. The data suggests that around 51% of OC-initiated CIRPs that were closed ended through appeal, review, or withdrawal, and that such matters accounted for more than 67% of all closures by appeal, review, or withdrawal. The underlying breakup is equally instructive. Of CIRPs initiated by OCs, 908 were closed on appeal/review/settlement and 853 were closed by withdrawal under section 12A. For FCs, the corresponding figures were 445 and 397 respectively, these numbers support a measured conclusion that a substantial portion of OC-led CIRP activity appears to culminate outside the full resolution-or-liquidation track, which also suggests that settlement dynamics continue to play a meaningful role in OC-led CIRP.

What the IBC System Has Actually Produced So Far

If initiation and closure patterns describe how different creditors use CIRP, the outcome shows what the system has produced at scale. IBBI states that the Code has rescued 4,002 corporate debtors, comprising 1,376 through resolution plans, 1,366 through appeal, review, or settlement, 1,260 through withdrawal. At the same time, 2,952 corporate debtors have been referred to liquidation.

For resolved corporate debtors, IBBI reports that realisation has been more than 31.63% of admitted claims, more than 171.54% of liquidation value, and 94.95% of fair value on average.

Realisation against liquidation value and fair value tells us that the process is often preserving and extracting value significantly better than a break-up liquidation baseline. But realisation against admitted claims remains far lower. It reflects that different benchmarks measure different things: one compares outcome against estimated asset value in liquidation, while the other compares outcome against the total claim pool.

A Structural Shift in the Making

It is fair to say that the IBC is increasingly reflecting a lender-led stress-resolution profile, especially in larger-default cases. It is also fair to say that operational-creditor usage remains concentrated in smaller-default matters, many of which continue to close through settlement-oriented routes rather than through the full insolvency pipeline.

The IBC’s current usage pattern appears to be moving closer to its institutional centre of gravity: larger-value, creditor-driven insolvency resolution, with operational-creditor, it is a meaningful inversion of its active user profile. In other words, the filing and closure data together point to a practical re-centering of CIRP around higher-value, institutional distress while OCs activity remains concentrated in smaller-default bands.

Conclusion

The latest IBBI data presents a clear message. Historically, financial creditors and operational creditors occupied almost equal ground in CIRP initiation. But in the Oct–Dec 2025 quarter, FCs accounted for 109 of 163 initiations, while OCs accounted for 44.

At the same time, IBBI records that about 80% of sub-₹1 crore CIRPs are OC-initiated, while about 80% of over-₹10 crore CIRPs are FC-initiated.

These figures suggest that the IBC’s filing base is becoming more strongly aligned with default size, creditor type, and the economics of resolution. It indicates that the IBC is increasingly functioning, at least in its more consequential cases, as a framework for institutional resolution of financial distress rather than a broadly interchangeable substitute for ordinary debt enforcement. And that, in the end, is what separates a bankruptcy framework from a routine payment-recovery lever: who invokes it, and for what objective.

The intricate relationship between contractual autonomy and the protective embrace of statutory remedies, particularly within the realm of consumer protection, has long presented a complex legal conundrum. While the freedom to contract allows parties to agree to resolve disputes through private arbitration, welfare legislation like the Consumer Protection Act establishes public fora, designed to safeguard consumer interests. A recent judicial […]

Introduction The immense fortunes generated by vast, illicit enterprises often rely on seemingly minor criminal acts—forgery, cheating, and conspiracy—to facilitate the flow of billions through a high-profile, unregulated activity like illegal sports betting. When the authorities finally move to dismantle such a racket and seize the wealth, a complex legal challenge emerges: Can the entire fortune be attached under anti-money […]

Introduction The controversy surrounding platforms like Sci-Hub and LibGen is more than a simple legal brawl over ‘piracy‘; it is the visible tremor of a far deeper structural fault line running beneath Indian academia. The real crisis is not the illicit downloading of papers, but the architecture of knowledge ownership itself: the virtually unquestioned legality of the zero-royalty copyright assignment […]