Can participation in corporate financial decision-making and overseas asset management amount to money laundering even without direct ownership of illicit assets?

That question arose before the Special Court in Directorate of Enforcement v. Punit Garg1, a bail proceeding emerging from investigations linked to Reliance Communications and its associated entities. The case required the Court to examine the scope of liability under Sections 3 and 4 of the Prevention of Money Laundering Act, 2002 (“PMLA”), particularly in the context of layered financial transactions, offshore corporate arrangements and alleged concealment of proceeds of crime.

The proceedings are significant because they reflect the judiciary’s increasingly stringent approach toward economic offences involving transnational transactions and complex corporate structures, where courts are focusing less on formal ownership and more on the broader economic role allegedly played in movement and concealment of disputed assets.

Investigations into Overseas Transactions

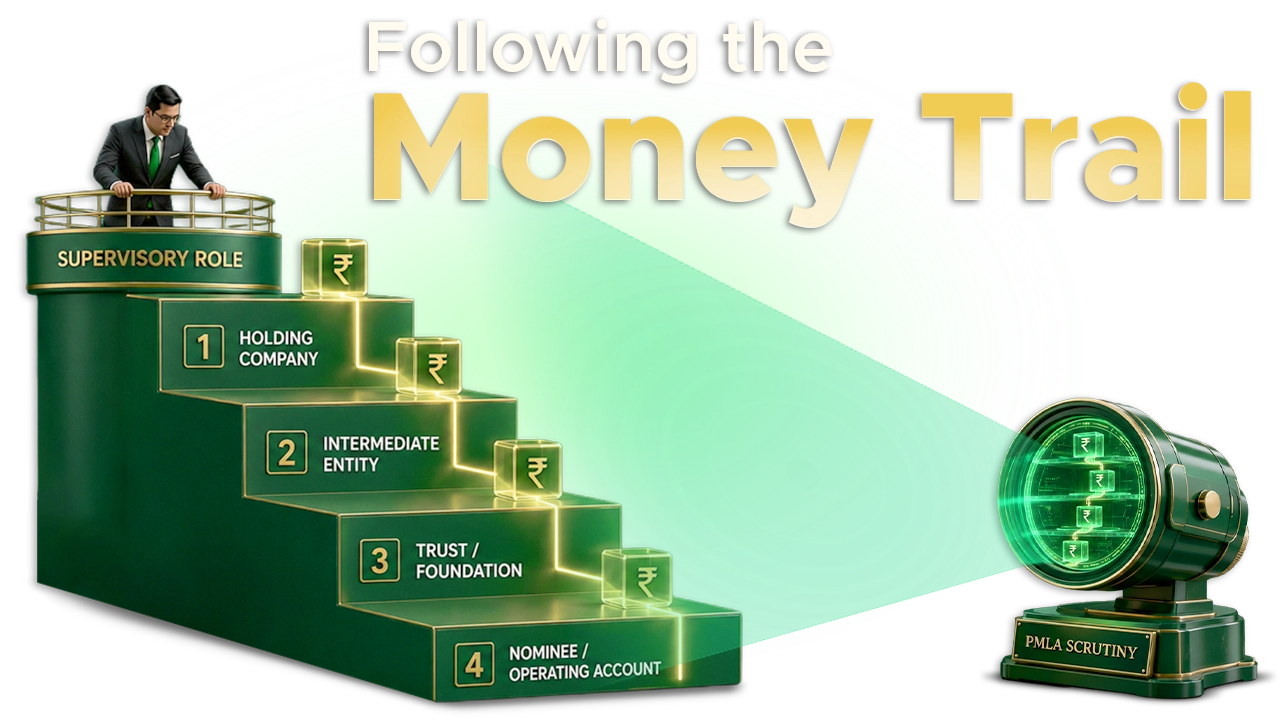

The proceedings originated from investigations conducted by the Enforcement Directorate (“ED”) into the alleged diversion of loans obtained by Reliance Communications and related entities from banks and financial institutions. According to the ED, portions of these funds were routed through overseas subsidiaries and utilised in transactions involving foreign assets and offshore corporate entities. The investigation particularly focused on transactions involving a Manhattan apartment and a luxury yacht “TIAN,” along with movement of sale proceeds through foreign financial arrangements.

The ED alleged that out of approximately USD 9 million generated from the sale of the Manhattan apartment, nearly USD 8.2 million was diverted and invested into AZCO Real Estate Brokers LLC, UAE. It was further alleged that company resources were utilised for payment of educational fees and personal expenses of the applicant’s daughters through the University of Southern California portal during 2017 and 2018.

Notably, the order reflected certain numerical inconsistencies regarding the alleged personal expenditure component. While one portion referred to expenses amounting to approximately USD 7700 and simultaneously equated the figure to nearly INR 49 lakhs, later portions referred to itemised transfers of USD 19,657.43, USD 36,560 and USD 20,829. Although the Court did not reconcile these figures at the bail stage, the discrepancy remains relevant from an evidentiary perspective.

Following investigation into these transactions, proceedings under the PMLA were initiated and the applicant approached the Special Court seeking regular bail after custodial interrogation and filing of prosecution complaints.

Rival Submissions before the Court

The defence argued that no direct material established the applicant’s involvement in generation of proceeds of crime or intentional concealment of illicit assets. It was contended that several disputed transactions predated the alleged scheduled offences and that many decisions concerning the assets were undertaken as part of insolvency-related processes involving lenders, boards and insolvency professionals.

A significant statutory argument raised by the defence concerned the applicability of the twin conditions under Section 45 of the PMLA itself. The defence argued that the only triable allegation directly connecting the applicant to personal enrichment involved amounts below Rs. 1 crore, approximately between Rs. 49 lakhs and Rs. 70 lakhs. Consequently, it was contended that the rigours of the twin conditions may not strictly apply in light of the proviso to Section 45.

The defence further argued that issues relating to corporate administration and financial management were being improperly transformed into allegations of money laundering without establishing a clear nexus between the applicant and the alleged tainted property.

The ED opposed the bail application by asserting that the applicant exercised supervisory influence over transactions involving overseas entities and disputed assets. The prosecution relied upon financial records, electronic communications and WhatsApp exchanges allegedly demonstrating involvement in transfer, utilisation and concealment of sale proceeds arising from foreign asset transactions. According to the ED, the allegations disclosed prima facie participation in layered financial arrangements involving proceeds of crime.

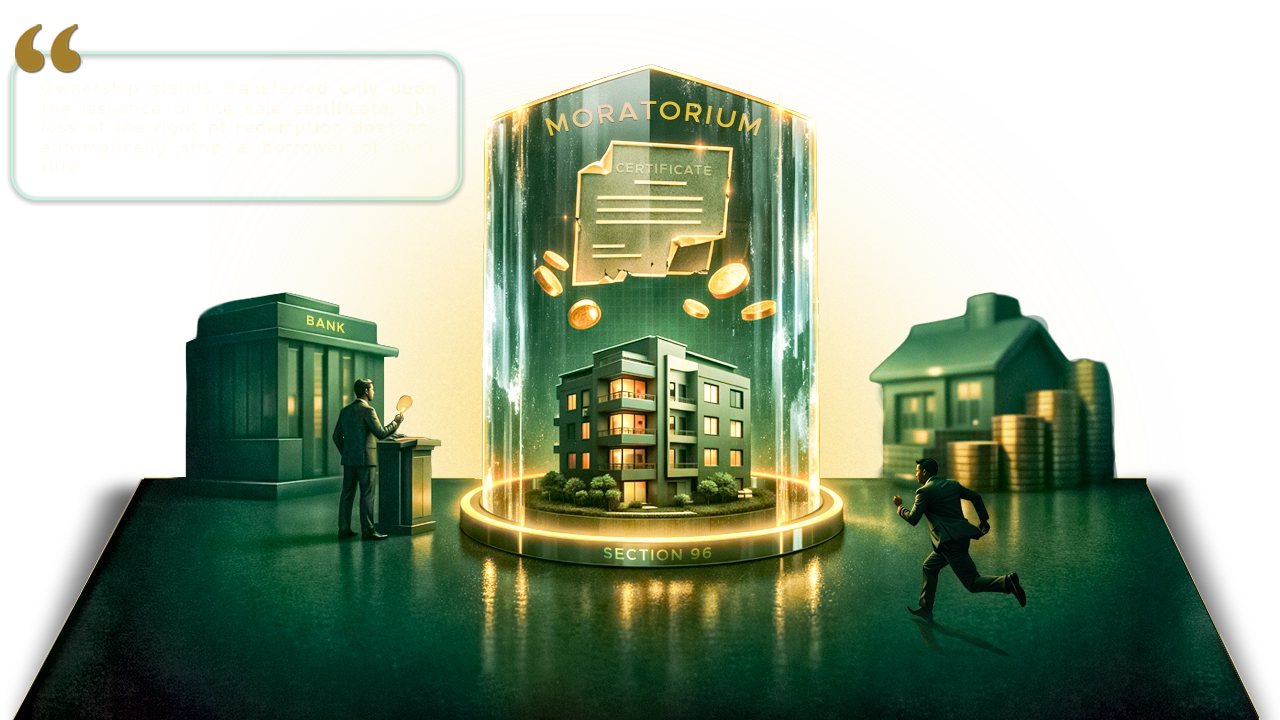

The prosecution also resisted attempts to shield the transactions behind corporate structures and insolvency proceedings. In this context, reliance was placed upon Varsanna Ispat Ltd. v. Deputy Director, Directorate of Enforcement2, where it was recognised that a moratorium under Section 14 of the Insolvency and Bankruptcy Code, 2016 does not bar attachment proceedings under the PMLA.

Court’s Findings and Judicial Reasoning

The principal issue before the Court concerned the restrictive bail framework under Section 45 of the PMLA, which requires an accused to satisfy the statutory “twin conditions” for grant of bail. While evaluating the application, the Court examined documentary material, financial records and electronic communications placed on record by the ED. Particular significance was attached to material allegedly demonstrating participation in overseas financial arrangements and handling of proceeds arising from disputed foreign assets.

In examining the scope of money laundering liability, the Court relied upon Vijay Madanlal Choudhary v. Union of India3, where the Supreme Court clarified that Section 3 of the PMLA extends beyond direct possession of illicit property to include concealment, use, projection or claiming of proceeds of crime as untainted property.

The Court also relied upon Rohit Tandon v. Directorate of Enforcement4, where the Supreme Court observed that economic offences involving layered financial transactions require a stricter approach because of their serious impact upon the financial system. Further reliance was placed upon Y.S. Jagan Mohan Reddy v. CBI5, where the Supreme Court recognised economic offences involving deep-rooted conspiracies and large-scale financial irregularities as a distinct category requiring a different approach in bail jurisprudence.

The Court additionally referred to P. Chidambaram v. Directorate of Enforcement6 while discussing the gravity of economic offences and Ranjitsing Brahmajeetsing Sharma v. State of Maharashtra7 on statutory restrictions governing bail under special criminal statutes.

After considering the material placed on record, the Court held that sufficient prima facie material existed connecting the applicant with transactions involving alleged proceeds of crime and their handling through overseas financial arrangements. The Court was not persuaded by the defence argument concerning the monetary threshold under the proviso to Section 45 and concluded that the applicant failed to satisfy the mandatory twin conditions under the PMLA. Consequently, the bail application was dismissed, though the Court clarified that its observations were confined to adjudication of bail and would not prejudice the trial.

Conclusion

The Punit Garg proceedings demonstrate the increasingly expansive scrutiny being applied to financial conduct within modern corporate structures operating across multiple jurisdictions. The ruling indicates that courts are willing to move beyond narrow examinations of formal ownership and instead assess the broader economic role allegedly performed in management, movement and concealment of disputed assets.

The judgment is also significant for its treatment of layered offshore arrangements, electronic communications and supervisory participation as potentially relevant indicators of money laundering liability under Sections 3 and 4 of the PMLA. Equally important is the Court’s recognition that insolvency proceedings and corporate structuring may not, by themselves, insulate transactions from scrutiny under anti-money laundering laws, particularly where allegations of diversion and concealment of funds arise.

Viewed more broadly, the ruling illustrates the judiciary’s continuing inclination to adopt a rigorous approach toward economic offences involving sophisticated financial structures, transnational transactions and complex corporate arrangements while interpreting the restrictive bail framework under the PMLA.

Citations

Expositor(s): Adv. Aparna Shukla, Intern Divyanshi Srivastava