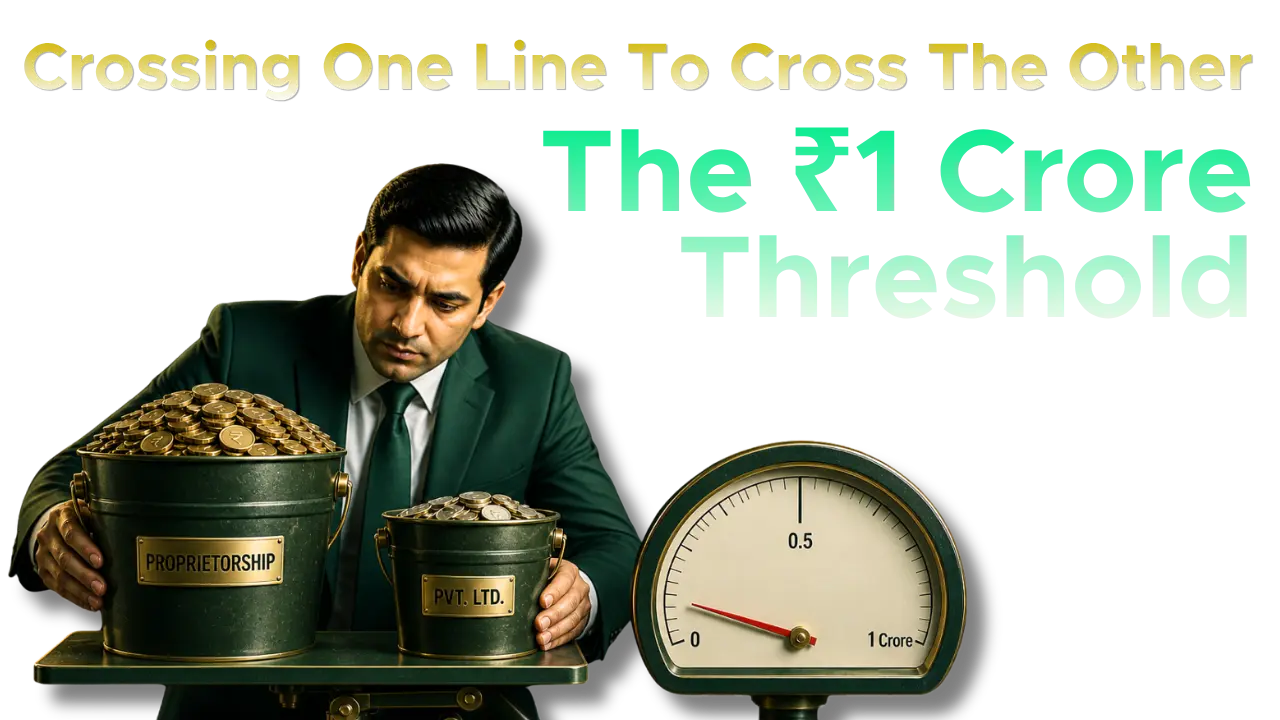

Can a creditor aggregate the debts of a sole proprietorship with those of a private limited company to meet the statutory ₹1 crore threshold under the Insolvency and Bankruptcy Code (IBC), simply because they share common management? In the matter of Bhushan Power & Steel Ltd. v. A.G. Pipes Pvt. Ltd1, the National Company Law Appellate Tribunal (NCLAT) totally rejected these contentions. The Tribunal affirmed that a corporate entity is a distinct legal person, and its liability cannot be artificially inflated by “loading” it with the debts of an independent proprietorship concern, even if both are operated by the same individuals. Consequently, if the debt specifically attributable to the Corporate Debtor falls below the limit prescribed under Section 4 of the Code, the petition must be dismissed as non-maintainable.

The Dispute Over Debt Aggregation

The Appellant, Bhushan Power & Steel Ltd. (BPSL), filed a Section 9 petition against A.G. Pipes Pvt. Ltd. (the Corporate Debtor), claiming a default of approximately ₹1.49 crores. BPSL contended that it had supplied steel products to the Respondent’s units and maintained two separate ledger accounts (SAP codes 1000224 and 1000579) for accounting convenience. BPSL further argued that the Respondent’s website listed both manufacturing locations one in Faridabad and one in Palwal under the same brand name. The Respondent, however, countered that “A.G. Pipes” (a sole proprietorship) and “A.G. Pipes Pvt. Ltd.” (a company) were separate legal entities with distinct GST registrations, PAN cards, and utility bills. They argued that the vast majority of the debt belonged to the proprietorship, and the amount owed by the Private Limited company was only ₹13,09,505 well below the ₹1 crore threshold.

Judicial Analysis and the Inapplicability of Precedents

The Tribunal’s rationale focused on the technical nature of IBC proceedings and the sanctity of corporate personality. The NCLAT observed that of the total operational debt claimed, approximately ₹1.42 crores pertained to the sole proprietorship, while only ₹13.09 lakhs was attributable to A.G. Pipes Pvt. Ltd. The Bench held that because the Private Limited company is a separate legal entity, its debts cannot be combined with those of another entity for the purpose of reaching the pecuniary threshold under Section 4. The Appellant’s attempt to justify the consolidation by pointing to a lack of “pre-existing dispute” was rejected as irrelevant to the foundational issue of maintainability.

The Appellant relied on several landmark judgments to support their claim, yet the Tribunal found them inapplicable due to the failure to meet the statutory threshold. Among these was Mobilox Innovations Private Limited vs. Kirusa Software Private Limited2, which is traditionally used to establish the “existence of dispute” test in Section 9 proceedings. Similarly, the Appellant cited Consolidated Construction Consortium Limited vs. Hitro Energy Solutions Private Limited3, a case dealing with the specific definition and scope of operational debt.

Further reliance was placed on M/s. Next Education India Private Limited v. M/s. K12 Techno Services Private Limited4 and Ahluwalia Contracts (India) v. Raheja Developers Limited5. Both of these cases reinforce the principle that for a dispute to be valid, it must be “pre-existing” meaning it must have existed before the receipt of the Demand Notice.

Despite these citations, the Tribunal concluded that these precedents could not cure a petition that failed to meet the basic statutory requirement regarding the minimum default amount. Because the debt attributable specifically to the Corporate Debtor fell below the ₹1 crore limit prescribed under Section 4 of the Code, the legal arguments regarding the nature of the dispute became irrelevant to the maintainability of the appeal.

Conclusion

The NCLAT’s decision reinforces that the IBC is not a tool for recovery and cannot be used to bypass the fundamental principles of corporate law. By dismissing the appeal, the Tribunal upheld the “Separate Legal Entity” doctrine, ensuring that the ₹1 crore threshold remains a strict barrier against the insolvency process being misused for smaller, aggregated claims. Ultimately, a creditor must prove that the specific corporate debtor, and no other associated entity, owes the minimum statutory amount before a Section 9 petition can be entertained.

Citations

Expositor(s): Adv. Jahnobi Paul